July 9, 2026

To manage finances properly, it’s important to understand how different payment methods affect cash flow. Even with the rise of digital transfers, many businesses still use paper checks. Handling them carefully helps avoid errors and audit problems. This guide provides a roadmap for handling business checks with operational efficiency.

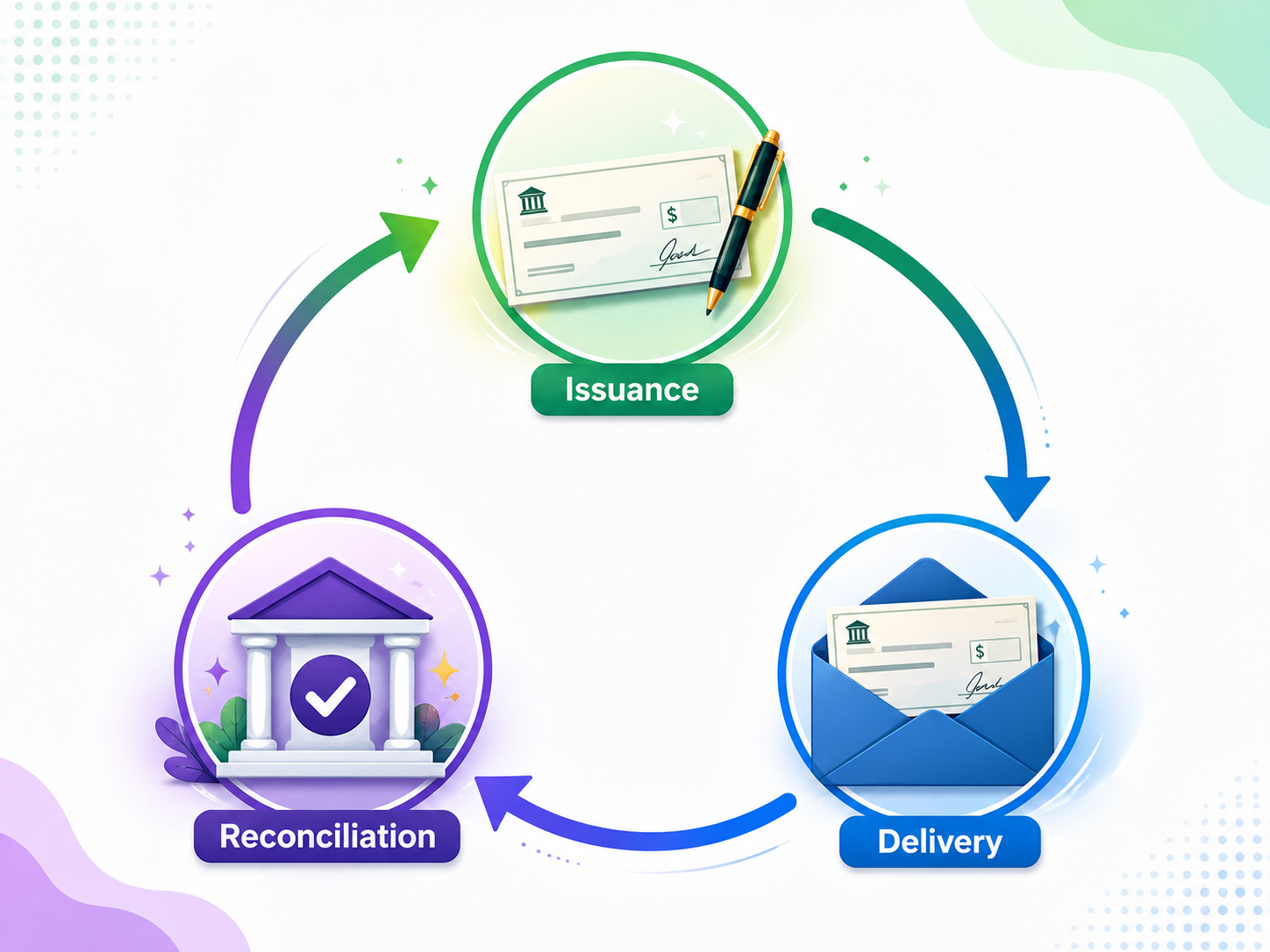

The process begins when a business authorizes a payment. Invoices should be verified against supporting documentation, such as approved purchase orders or contracts. Once verified, the check can be generated using accounting software. Every check typically includes a unique serial number for accurate internal tracking. You should record the payee name and the exact amount immediately.

Verify the Payee— Check the legal name of the payee.

Confirm the Amount—Make sure the written and numerical figures match perfectly.

Sign the Check—Use a secure signature from an authorized company officer.

Finalize in Software — Mark the check as "printed" in your system to confirm it has been issued and ensure accurate recordkeeping.

The next stage involves the physical or digital delivery of the document. You must make sure the check reaches the intended recipient on time. If you want a verifiable record of delivery, consider using a trackable option such as USPS Priority Mail, First Class Mail, Ground Advantage, or Certified Mail. Once the recipient receives the check, they will present it for payment. Your bank then processes the check through standard clearing systems.

The final stage of the lifecycle is the formal bank reconciliation process. Your bank records will reflect when funds leave your business account. Match the cleared check against your internal ledger using your bookkeeping software. This step confirms that the bank processed the correct amount for the payee. Any discrepancies must be investigated and resolved by your accounting department immediately.

Outstanding checks are payments that have been issued but not yet cashed. These uncashed checks can distort your reported cash balance and complicate reconciliation. You should review your outstanding checklist at least every thirty days. Identifying these pending items early prevents significant cash flow surprises later on. Maintaining a cash reserve can help cover outstanding obligations.

Review Monthly—Check your bank statements against your list of issued payments.

Flag Old Items—Any check older than thirty days deserves a closer look.

Update Forecasts— Adjust your available balance to reflect these pending withdrawals.

Identify Trends—Look for specific vendors who consistently delay their bank deposits.

If a check remains uncashed after sixty days, you should contact the payee. There is a high chance the check was lost or never delivered. You may need to issue a stop-payment order before writing a new check. This protects your business from the original check being cashed later. Consistent communication with your vendors makes sure that your accounts remain clean.

You must also be aware of state laws regarding unclaimed property. Many jurisdictions require businesses to report unclaimed funds after a defined dormancy period. This process is known as escheatment and involves turning funds over to the state. You can reduce compliance risk by resolving outstanding items well before applicable state dormancy deadlines. Keep a detailed log of all attempts to contact the original payee.

A common retention period for business check records is up to seven years, depending on applicable tax and regulatory requirements. This timeframe satisfies the requirements set by federal tax and labor authorities. You must keep records of both issued checks and those you receive. These documents are essential if your business faces a formal financial audit. Having organized records allows your team to respond to inquiries quickly.

Tax Compliance—The IRS may request proof of payment during a routine audit.

Audit Trails—Clear records demonstrate high levels of internal financial control.

Legal Protection—Checks serve as evidence of payment in any contractual dispute.

Loan Applications—Lenders often review past payment history during the approval process.

Many businesses have moved toward a digital-first archiving strategy. Since banks typically provide digital images of cleared checks, there's generally no need to create duplicates. Rely on your bank's records and ensure that digital files are stored securely, with proper backups, to prevent data loss.

Modern technology has significantly simplified the way businesses handle traditional paper checks. Mobile deposit applications allow you to scan and process incoming payments instantly. These tools use optical character recognition to capture key check data. You no longer need to visit a physical bank branch for deposits. This convenience can save your administrative team several hours every week.

You can also implement automated check-writing software within your existing workflow. Such platforms integrate directly with your online business checking accounts. They automatically assign check numbers and record the purpose of each payment. This automation reduces the risk of human error during the data entry phase. You can also set up multi-level approvals for all high-value payments.

Real-time fraud detection tools are another essential asset for businesses. These systems monitor your accounts for any suspicious or unauthorized check activity. They can flag checks that deviate from your typical spending patterns immediately. You will receive an instant alert on your mobile device for review. Implementing these digital safeguards protects your capital from sophisticated forgery and theft.

A hybrid payment strategy offers both traditional security and modern digital efficiency. You can link every physical check number to a specific digital invoice. This creates a transparent audit trail that is very easy to follow. Use unique identification codes to sync your paper records with cloud files. This method makes sure that your financial data stays organized and accessible.

Link Invoices—Attach a digital copy of the invoice to the check record.

Use Tags—Label entries with project names or specific department codes.

Sync Accounts—Make sure your bank feed matches your internal software daily.

Cloud Access—Allow your accountant to view check records from any location.

This automation feature cuts down the need to manually reconcile every bank account at month-end. It matches transactions automatically and flags anything that needs attention. You can also see your current balance clearly, which helps with cash flow and planning.

A well-organized digital system makes it easy to locate checks and payment records when needed. Tag each entry with relevant details such as vendor name, project, or department. This allows you to quickly generate spending reports, respond to audits, or provide documentation to stakeholders without digging through paper files.

Managing business checks is about choosing the right tool for the right moment. While instant payments have their place, checks remain unmatched when control and a clear paper trail matter most.

TechChecks provides secure, fully customizable business check solutions designed for organizations that understand the value of payment integrity. Because when it comes to your finances, the way you manage the details says everything about how you run your business.